For many HR leaders in Hong Kong, this renewal season is prompting a more fundamental question: is the traditional group medical model still the right structure for outpatient cover, or is there a better way to manage cost, visibility, and employee experience at the same time?

Key Takeaways

- APAC medical inflation reached 11.3% in 2026, the highest of any region globally, making this renewal season a turning point for Hong Kong employers absorbing another year of premium increases with no structural change.

- A self-funded outpatient plan replaces the fixed insurance premium with a per-employee budget: the employer pays only for outpatient services employees actually use, with real-time spend visibility replacing opaque, year-end insurer reports.

- Compared to traditional group medical, the self-funded model delivers direct cost control, category-level claims data, and the flexibility to configure allocations by employee grade or cohort, advantages that compounding premium inflation makes increasingly hard to ignore.

- The split model (group medical for inpatient, self-funded for outpatient) suits most enterprise employers in Hong Kong and is where the strongest ROI case sits; both require a PDPO and ISO 27001-certified platform to work.

If your group medical renewal quote has landed and it is higher than last year, you are not alone. APAC medical inflation reached 11.3% in 2026, the highest of any region globally, according to the Aon 2026 Global Medical Trend Rates Report. For employers renewing in the May-July window, that figure translates directly into double-digit premium increases with no structural change to what employees actually receive.

This guide walks through both options clearly, so you can make the right call for your workforce and your budget.

How Group Medical Insurance Works in Hong Kong

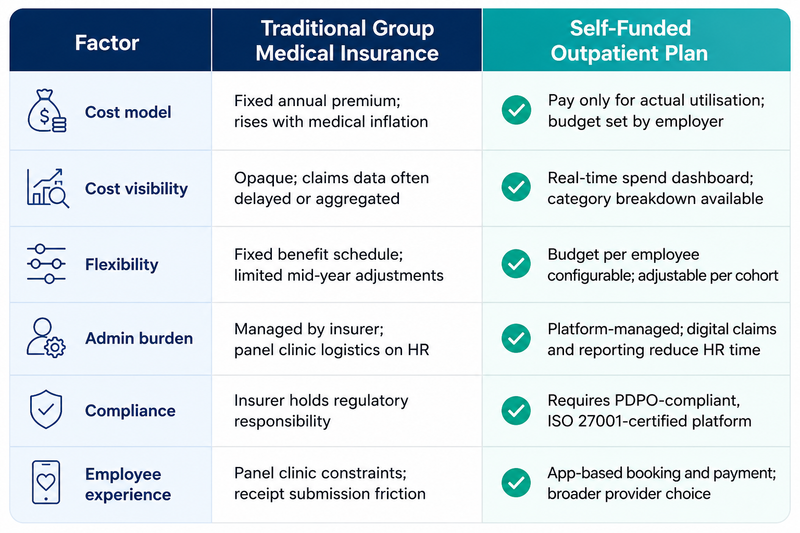

Group medical insurance in Hong Kong is the dominant model for employer-sponsored outpatient cover. The employer pays a fixed annual premium to an insurer. Employees visit a panel clinic or submit receipts for reimbursement up to defined limits. The insurer pools risk across the group and manages claims administration.

For inpatient cover, it remains the standard for good reason. For outpatient, the economics have shifted. Premium costs rise every year regardless of actual utilisation, and most employers have limited visibility into how their plan is being used. Data consistently shows that a significant share of employees do not make a single outpatient claim in a given year. Employers are paying for coverage that large portions of their workforce never access.

The Gaps in Traditional Group Medical

- No claims data. Insurers aggregate or delay claims reporting; employers often see little more than total utilisation figures at year-end with no category breakdown. Without line-item visibility, it is impossible to identify where spend is concentrated or whether the plan is working for the workforce.

- Inflexibility. Fixed benefit schedules offer limited ability to adjust mid-year; allocations cannot easily be varied by employee grade, role, or cohort. Employers running multi-level or multi-location workforces are particularly constrained by a structure designed for uniform coverage.

- One-size-fits-all cover. Every employee receives the same plan regardless of their actual health needs or preferences. There is no personalisation: the junior analyst and the senior director draw from identical benefit limits, regardless of how their healthcare needs differ.

- Preventive care is underserved. Panel clinic models are built around reactive treatment, not prevention. Wellness visits, mental health support, and allied health services are often excluded or heavily capped, leaving a growing category of employee health need unaddressed within the plan.

- Premiums do not reflect actual usage. The pooled model means employers with low-utilisation workforces subsidise higher-utilising cohorts. Claims history rarely translates into proportionate premium savings at renewal; the insurer's pricing reflects portfolio risk, not your group's specific record.

What Is a Self-Funded Outpatient Plan in Hong Kong?

A self-funded outpatient plan (also referred to as an employer-funded or direct-funded outpatient programme) replaces the insurance premium model with a defined budget structure. The employer allocates a defined annual outpatient budget per employee. Employees spend from that budget directly, with approved claims settled digitally. There is no insurance underwriting, no risk pool, and no markup built into the pricing.

In practice, the employer pays only for outpatient services employees actually use. If an employee uses HK$3,000 of a HK$5,000 annual allocation, the employer's cost is HK$3,000, not a fixed premium calculated on assumed utilisation across the group.

The employer absorbs cost risk directly rather than transferring it to an insurer. The model suits employers with stable, predictable workforces where actual outpatient utilisation is knowable and real-time spend data is available to inform decisions.

Whether a self-funded outpatient plan is practical to run comes down to the platform behind it. Without a compliant, digital-first system handling claims, tracking, and reporting, the admin burden falls back on the HR team.

Side-by-Side Comparison

How the two models compare across six key factors

Which Approach Suits Your Organisation?

Large enterprises seeking cost control and spend transparency

If your organisation has 500 or more employees and your benefits team is receiving renewal quotes 10 to 15 percent above the prior year, a self-funded outpatient plan gives you a direct line of sight into what is actually being spent and where. You can set budget allocations by employee grade or cohort, monitor utilisation through a real-time dashboard, and make evidence-based adjustments at renewal rather than reacting to insurer pricing with limited data. The model works best when you have the workforce scale to make utilisation data meaningful and want to move from cost absorption to cost management.

Employers with low outpatient utilisation in their current plan

If your analysis of existing group medical data shows that a material portion of your workforce is not submitting outpatient claims, you are paying a pooled premium that does not reflect your actual group risk. A self-funded structure resets that equation. You allocate a per-employee budget and pay on utilisation. An employer that previously subsidised a high-utilisation minority through flat-rate premiums now pays based on what the whole group actually does.

Organisations wanting to retain group medical for inpatient but modernise outpatient

The two models are not mutually exclusive. Many employers in Hong Kong maintain group medical insurance for hospitalisation and surgical cover, where risk-pooling remains a sound approach for low-frequency, high-cost events, while moving outpatient to a self-funded structure. This split design gives employees comprehensive cover for serious health events while giving the employer direct control over the higher-frequency, lower-cost outpatient spend that drives annual premium inflation.

What Makes a Self-Funded Outpatient Programme Work

The operational execution depends on the platform behind it. Without a certified, digitally-integrated system, the admin that the insurer previously handled falls to the HR team, employees face friction when accessing their benefits, and the spend visibility that justifies the model in the first place never materialises.

When evaluating a platform for a self-funded outpatient programme in Hong Kong, four requirements matter most: PDPO and ISO 27001 certification (baseline data privacy and security standards for employer-held employee health data in HK); a real-time spend dashboard giving HR and finance live utilisation and budget visibility; digital claims settlement so employees are not managing paper receipts; and a mobile-first employee experience that makes benefit access straightforward.

That is how MixCare Health's Self-Funded Outpatient product operates. Employers set the annual outpatient budget per employee. Employees book providers and pay through the MixCare app, with claims settled digitally. The employer sees real-time utilisation data, category breakdowns, and budget status in a single dashboard. There is no insurance markup, and there are no opaque pooled costs. The platform is certified under PDPO (HK) and ISO 27001, with independent annual security testing. It was built for the Hong Kong market, not adapted from a global product.

If renewal is on the desk and the cost of doing nothing is another double-digit premium increase, the model is there to change it. MixCare's Outpatient Budget Calculator lets you run the numbers before committing to anything: enter your headcount, current premium per head, and estimated utilisation patterns to see your projected cost under a self-funded structure set against your renewal forecast. The platform behind it handles claims, reporting, and employee access from day one.

Ready to see how a self-funded outpatient programme works for your team?

MixCare Health works with HR leaders at enterprise organisations across Hong Kong to design, configure, and manage self-funded outpatient plans, with full compliance and real-time spend visibility built in. No commitment required.

Frequently Asked Questions

What is a self-funded outpatient plan in Hong Kong?

A self-funded outpatient plan is an employer-sponsored benefits structure where the employer allocates a defined annual outpatient budget per employee instead of paying a fixed group insurance premium. Employees spend from that budget for outpatient care, and the employer pays only for actual utilisation. The model gives employers direct cost control and real-time visibility into outpatient spend.

How does a self-funded outpatient plan differ from group medical insurance?

Traditional group medical insurance pools risk across the workforce and charges a fixed annual premium, regardless of actual utilisation. A self-funded outpatient plan eliminates the insurance markup and pooled premium structure. The employer funds outpatient costs directly and sees exactly how and where the budget is being used, rather than receiving aggregated claims data from an insurer at the end of the year.

Is a self-funded outpatient plan compliant with Hong Kong's PDPO requirements?

It depends on the platform. Because a self-funded outpatient programme involves the employer handling employee health data directly, the platform managing claims and utilisation must be PDPO (Personal Data Privacy Ordinance) compliant. MixCare Health is both PDPO-certified and ISO 27001-certified, with annual independent security testing. Employers should confirm these certifications with any platform they evaluate.

Can a self-funded outpatient plan work alongside existing group medical insurance?

Yes. Many Hong Kong employers retain group medical insurance for inpatient and surgical cover, where risk-pooling is most valuable, while implementing a self-funded structure for outpatient. This combined approach preserves comprehensive cover for high-cost health events and gives the employer direct control over outpatient costs, which is where annual premium inflation is typically highest.

Which employers benefit most from a self-funded outpatient plan in Hong Kong?

Employers with 500 or more employees who are experiencing significant group medical premium increases, have limited visibility into outpatient utilisation, or want to move from a flat-premium cost structure to one that reflects actual workforce health spend are well-positioned to benefit. The model is most effective when managed through a certified digital platform that handles claims, reporting, and employee access in one place.

MixCare Health

MixCare Health · Hong Kong